HIMS: Growing Into Its Valuation and My Updated Price Target

Q1 2025 Earnings and Valuation Updates

For a review on HIMS as a company and my thesis see my original post at: HIMS: Redefining Personalized Healthcare & Scaling for the Future

My initial post HIMS: Redefining Personalized Healthcare & Scaling for the Future laid out my thesis for HIMS as a disruptive healthcare brand with strong multi-bagger potential. Since that post on 3/23 a lot has happened and HIMS has just about doubled… and I feel strongly that we are just getting started. Let me start by making it clear - I don’t think HIMS is short-squeezing (or care if it is), I think HIMS is re-rating and growing into its true intrinsic value.

Financial Metrics (as of 5/19/25):

Price: $62.34

Market Cap: $13.93 billion

Shares: ~223 million, fully diluted: ~246 million

FCF/Share: 1.11

FCF Yield: 1.79%

SBC Adjusted FCF/Share: 0.66

SBC Adjusted FCF Yield: 1.06%

Forward FCF/Share = 1.22

FWD FCF Yield: 1.96

FWD EV/Sales: 5.77

Price/Sales: 8.11

FWD Price/Sales: 5.88

Q1 2025 Earnings Highlights:

HIMS continues to deliver. As discussed in my initial HIMS post, one of the largest risks facing the company post-GLP1 shortage was execution risk. Facing increased scrutiny, HIMS needed to deliver and needs to continue to deliver strong results to push through the negative sentiment overhang and establish confidence in the company's financial success without Commerical GLP-1. In Q1 2025, HIMS did just that with outstanding growth metrics across the board.

Revenue Growth: 111% YoY

Net Income: 345% YoY

Operating Cash Flow Growth: 322% YoY

**Free Cash Flow Growth: 322% YoY (**Note: HIMS applies a conservative approach, including web and app development in FCF calculations. Numbers may differ from DCF calculations in the valuation section.)

Subscriber Growth: 38% YoY

Monthly Online Revenue per Avg. Subscriber: $84, 53% YoY

Regarding Subscriber Slow-Down

Per HIMS Shareholder Letter, subscribers increased 38% YoY from 1.7m in Q1 2024 to 2.4m in Q1 2025. However, the actual number for Q1 2025 is 2.366 million and the actual number for Q4 2024 is 2.23 million. While still impressive, some concern has arisen regarding the QoQ growth of only 136,000 or 6.1% which is a deceleration and is the company’s lowest QoQ subscription growth rate.

While not ideal, there are a few things in play. First, the GLP-1 shortage was declared resolved on February 21, 2025. This resulted in an end to HIMS ability to sell non-personalized GLP-1s. As such, while some of those subscribers that were pure commercial GLP-1 subs were undoubtedly transitioned to alternative HIMS weight loss offerings, a large percentage is assumed to have transitioned off of the HIMS platform to seek GLP-1 via other commercial providers. This has resulted in a greater number of subscriber exits in Q1 and lower total net new subscribers. This was expected and is not concerning news to me. CEO Andrew Dudum helped to set that expectation in the Q4 Conference Call.:

Obviously, we have the expansive platform, whether it's the oral medication that are already out there or if there is some reason that this patient would qualify for some level of personalization that exists. But I would suspect, just being very direct, that a lot of those patients will try to go into the open market and try to secure a branded option in some form factors. So that transition is inevitable. I think that transition is going to have to take place and has been built into the guidance that Yemi provided.

Second, when high growth companies grow, the law of large numbers comes into play and while net subscriber additions have remained consistent for the most part, reported growth rates will begin to reflect deceleration as the denominator becomes bigger. HIMS is not only adding a significant number of new subscribers, but it is rapidly increasing the Monthly Avg Revenue per Subscriber added.

Regarding the expected Q2 Slowdown and Margin Compression

HIMS has never been a GLP-1 company but it did make a strategic investment in entering the compounded GLP-1 space during the semaglutide shortage. From the beginning though, HIMS expected the shortage to come to an end. Yet, the decision was made to heavily invest in targeted marketing to bring in new weight loss consumers via GLP-1 to the HIMS & HERS ecosystem. This investment resulted in increased subscriber growth, increased branding, and increased revenue. However, it also resulted in compressed margins and has led to the inevitable first expected drop in sequential quarter revenue. These inevitable outcomes have been noted repeatedly during earnings calls to help set the stage and temper expectations. This should have been an expectation, not a concern.

See insight from Yemi regarding the upcoming expected decrease in revenue and color on current gross margin compression:

This transition is expected to result in a one-time quarter-over-quarter revenue drop in the second quarter, from which we are confident we can continue to build upon through the remainder of the year. Third, we expect gross margins to expand in the second quarter.

Gross margins declined approximately three points quarter-over-quarter as GLP-1 revenue scaled.

I think on gross margins, we do expect those to sequentially increase. I think as we look into the ecosystem we see a couple things. One is just a benefit from economies of scale. The second is we do expect strength and growth outside of our GLP-1 offering, which historically has come at a different margin profile currently, to also start to elevate the gross margin profile as we progress over the course of the year.

HIMS has repeatedly guided that long-term gross margin targets were “mid 70s.” Thats where we are now…

If you're finding this content valuable, consider subscribing and sharing it with someone who might benefit.

You can also support me by buying me a coffee at: buymeacoffee.com/manuinvests!

Valuation

Keep in mind that all of my calculations are estimates, intended to provide general guidelines for my personal decision-making.

Let’s Review…

In my initial HIMS write-up, I provided some valuation insight using a Price/Sales Multiple Valuation model. In this model, I used company guidance regarding the goal of reaching 10 million subscribers and applied the FY2024 Average MARPU to reach a range of 2031 price estimates.

At the time, my conservative estimates were:

And my ‘base bullish’ estimates were:

Using a bullish yet reasonable P/S ratio of 7.5 brought both scenarios to…

Let’s Update…

If you look at the valuation range, the mid-point was around $6.05 billion in revenue. This falls pretty in line with management’s long-term guidance of “2030 revenue of at least $6.5 billion.” I actually think my bullish estimates are still more realistic as HIMS has a history of lowballing guidance (HIMS has a 100% guidance beat record) and reached their 2025 LT guidance goal a full year early.

Let’s update our model first by bringing it to 2030 to determine CAGR from current price. My initial estimates used 2031 to be conservative but let’s follow managements target of 2030. Also, note I am not updating the MARPU to increase as I would like to remain conservative and feel GLP-1 may have temporarily elevated monthly revenue rates in Q1.

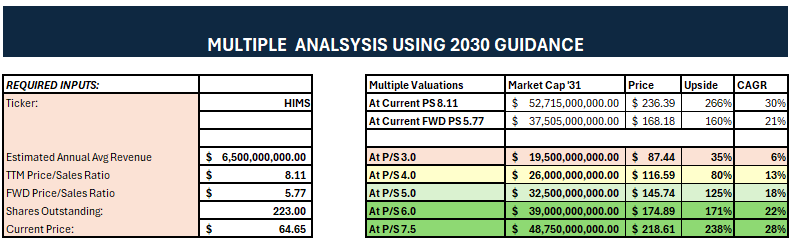

CEO scenario: 2030 at least $6.5 billion in revenue:

Implied 2030 Price Range: $87.44 - $218.61. Average: $148.65

Implied Upside from current price: 35% - 238%. Average: 130%

Implied CAGR: 8% - 28%. Average: 17%

Price for 3x Upside (~200% Gain): ~$49.55

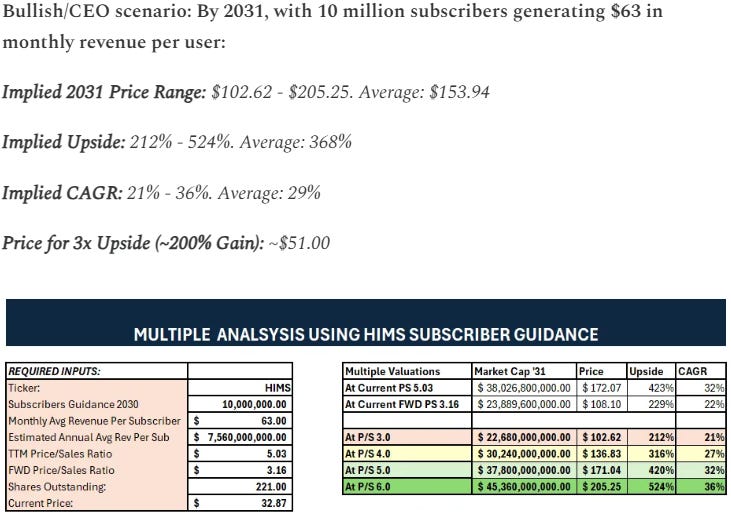

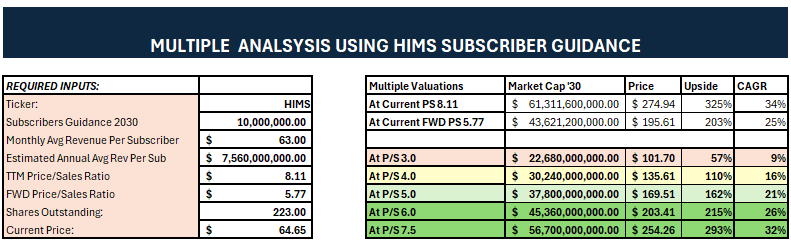

Bullish scenario update based on prior estimates: 2030, with 10 million subscribers generating $63 in monthly revenue per user:

Implied 2030 Price Range: $101.7 - $254.26. Average: $172.90

Implied Upside from current price: 57% - 293%. Average: 167%

Implied CAGR: 9% - 32%. Average: 21%

Price for 3x Upside (~200% Gain): ~$57.63

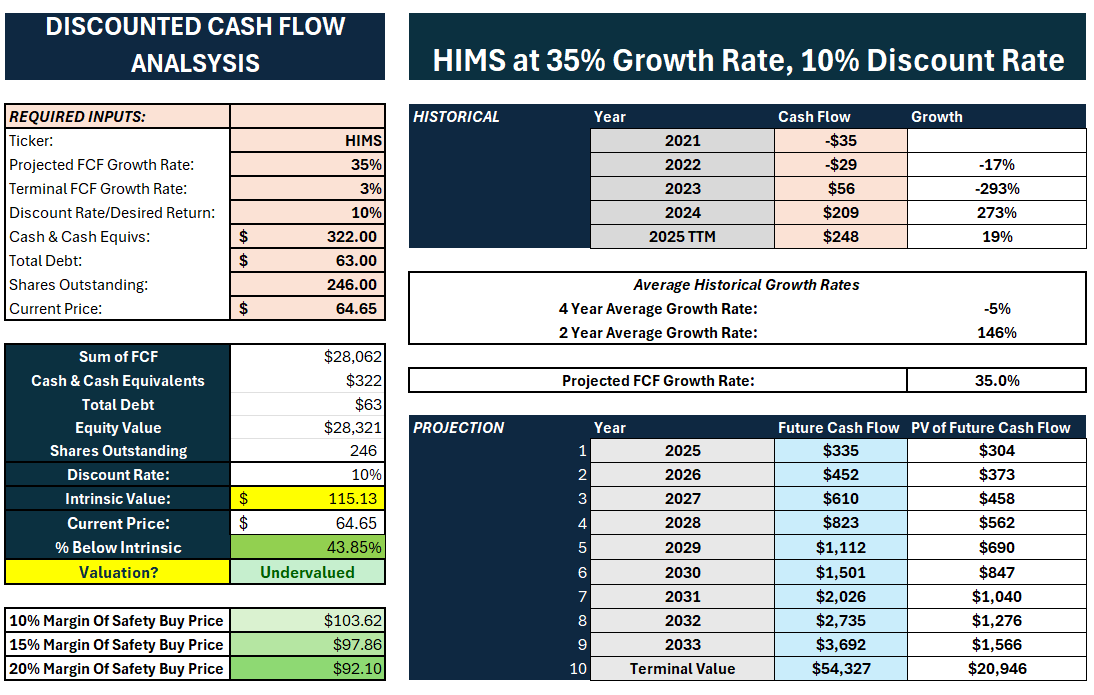

Discounted Cash Flow

*I have increased shares outstanding to represent the fully diluted potential share count.

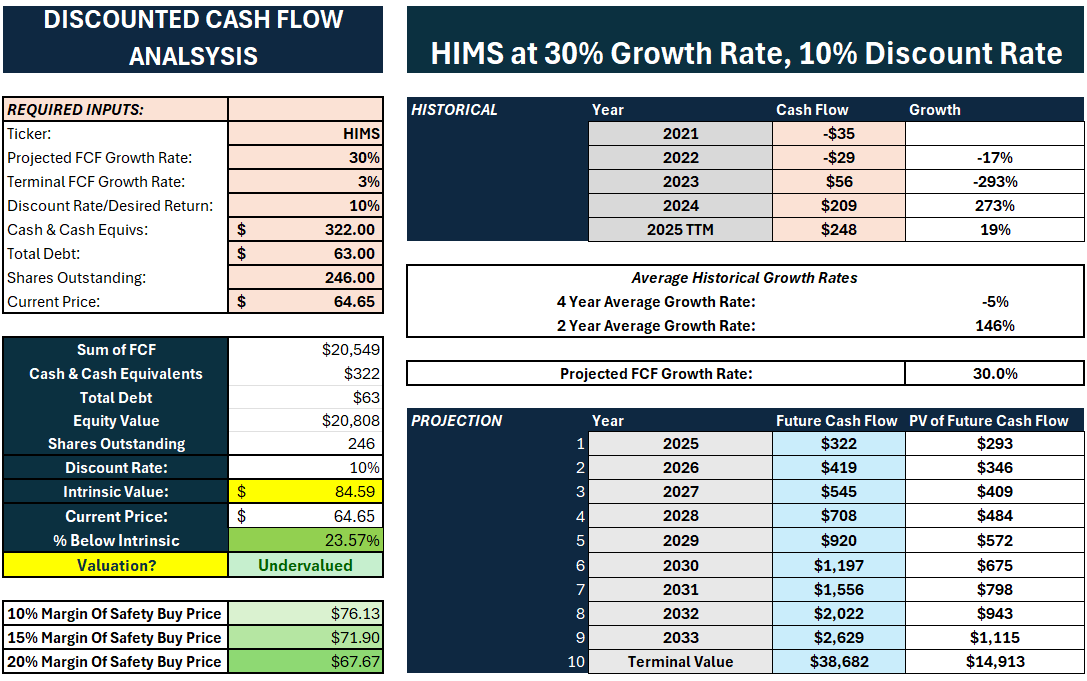

At 35% Free Cash Flow Growth Rate, Terminal 3%. Reflects undervalued.

At 30% Free Cash Flow Growth Rate, Terminal 3%. Reflects undervalued.

At 25% Free Cash Flow Growth Rate, Terminal 3%. Reflects at fair value.

*Note: HIMS is growing FCF at 321% YoY… See note below DCF Calculations for further insight.

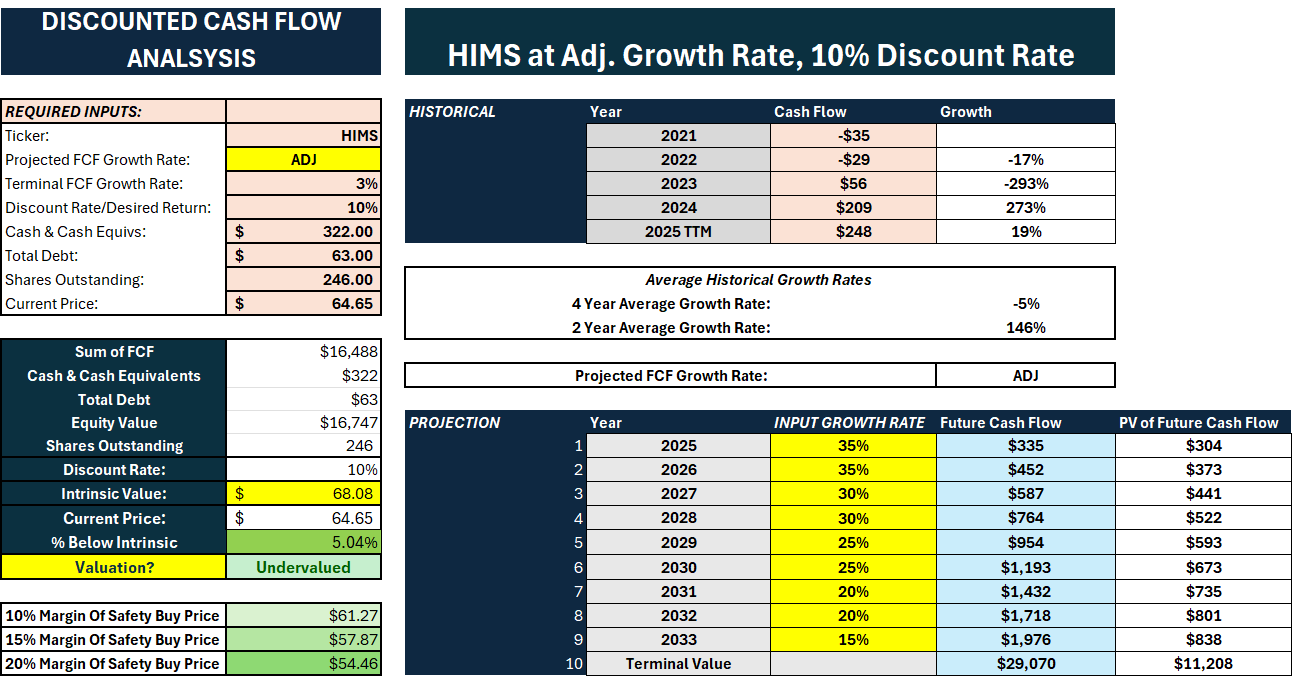

At 35% Decelerating to 15% Free Cash Flow Growth Rate, Terminal 3%. Reflects undervalued.

Regarding *Note: HIMS is growing FCF at 321% YoY… The 25% growth rate, in particular, is an extremely conservative rate to help ground the range of potential outcomes for HIMS. By front loading the FCF growth with a single year at 50% before falling to 25%, the intrinsic value would jump to $73.93.

While it is always difficult to predict multiple years of FCF, I believe these growth rates all fall on the conservative side and provide an additional margin of safety in the calculation as 1-2 years of mid-to-high double digit or triple digit growth rates will significantly front load much of the growth required to reach any of these outcomes.

DCF Valuation Summary:

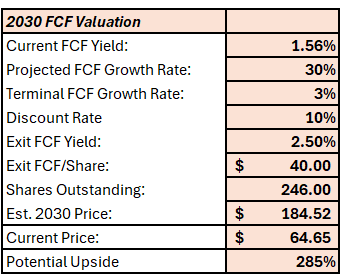

We can also look at FCF through the lens of the company’s recent guidance for 2030 using Adj-EBITDA as a reasonable proxy for cash. The company guided for “2030 Adjusted EBITDA of at least $1.3 billion.” This lines up pretty well with my 30% growth rate and 35% to 10% decelerating growth rate model which both result in approx. $1.1 billion in FCF in 2030. HIMS current FCF Yield is 1.56%.

If we assume some multiple compression to 2% and apply a P/FCF to our 2030 projected/guided FCF of $1.1 billion we get a potential price of $230.65.

If we assume greater multiple compression to 2.5% we get a potential price of $184.52.

If we add in some assumed dilution of 4% a year, we end with prices of $209.37 and $167.50 respectively.

Updated Thoughts on Valuation:

A lot has happened in the last few months. I have ridden this price roller coaster up and down multiple times, but I continue to hold and have significantly added to my position at opportune valuations. In my last HIMS post, I noted that “I view $46.64 and below as an attractive price,” and after Q1 earnings my conviction has only increased. I most recently added a small allocation at $46.10 following earnings.

As I noted above, in my opinion HIMS recent run up is the stock growing into its fundamental valuation, not past it. If HIMS can continue to deliver I think we have a lot of room left to run and I am excited to see what is to come.

For now - I believe a pretty conservative intrinsic value for HIMS is in the range of $68 - $85. I am not considering any short-term actions other than holding. I genuinely feel these ranges are conservative but due to the inherent unpredictability of such a high-growth, volatile stock, I am attempting to remain reasonably grounded in my assumptions as I would prefer a larger Margin of Safety and Suprise to the upside rather than downside.

Regarding the company’s 2030 guidance and my 2030 models - I don’t think a 3x from here is out of the question. That would be a 6x since my last write up.

HIMS currently accounts for a significant sizing in my portfolio. However, I will be adding more if the stock drops below $50. Based on a 20% margin of safety using a 25% free cash flow growth rate discounted at 10%, I view $49.00 and below as an attractive price for my portfolio.

Hope this helps and hope you have some HIMS gains!

If you found this content helpful, please consider supporting with a paid subscription or by buying me a coffee at: buymeacoffee.com/manuinvests

Get a copy of my Valuation spreadsheet: Fundamentally Sound Valuation Spreadsheet

Disclaimer: The content shared on Fundamentally Sound is for informational and educational purposes only and should not be considered financial advice. Please do your own research before making any investment decisions.

Great article. Thanks for sharing.

I think by and large the HIMS long investment community has a blind spot and missing significant red flag: the deceleration of the growth for the Core (excluding GLP1) business and in particular the Legacy (excluding all weight-loss) business.

For FY25 the company has effectively guided for Core to grow by 49% over 2024, yet in Q1, using public disclosures, we can estimate core slowed even further to 28% growth.

It's worse for Legacy (excluding all weight loss). They effectively guided for 43% growth in FY25, but Q1 (again, with public disclosures), we can estimate Legacy growth slowed down to 15%.

Consequently, HIMS' growth prospects are too dependent on GLP1 growth and *any* news (e.g., Cigna) that puts GLP1 revenue at risk *will* (rightfully so) move the stock price.