HIMS: Redefining Personalized Healthcare & Scaling for the Future

A premium consumer experience with strong valuation growth: HIMS’ approach to personalized care and financial success.

Business Overview

Hims & Hers is the leading health and wellness platform on a mission to help the world feel great through the power of better health. Hims & Hers Health is a founder-led, telehealth company that provides personalized healthcare and wellness solutions through a direct-to-consumer model. The company offers access to medical consultations, prescription treatments, and over-the-counter health products across various categories, including sexual health, mental health, weight loss, hair loss and more.

Financial Metrics (as of 3/21/25):

Price: $32.87

Market Cap: $7.44 billion

Shares: ~221 million

FCF/Share: .93

FCF Yield: 2.69%

SBC Adjusted FCF/Share: .50

SBC Adjusted FCF Yield: 1.44%

Forward FCF/Share = 1.29

FWD FCF Yield: 3.9

FWD EV/Sales: 3.01

Price/Sales: 5.03

FWD Price/Sales: 3.16

Potential Concerns Addressed Below:

Ending of the semaglutide (GLP-1) shortage by FDA.

Growth ex-GLP-1.

No moat?

Share dilution.

Company Highlights:

Incredible Growth:

Revenue: +95% QoQ, +69% YoY

Free Cash Flow: +452% QoQ, +322% YoY (Note: HIMS includes web & app development in FCF CapEx calculations)

Over 90% of revenue comes from recurring subscriptions.

Rapid revenue growth and operational efficiency is driving profitability.

Clean balance sheet, $300M+ in cash, no long-term debt.

Capital light business model providers opportunity for increased operating leverage and margin expansion.

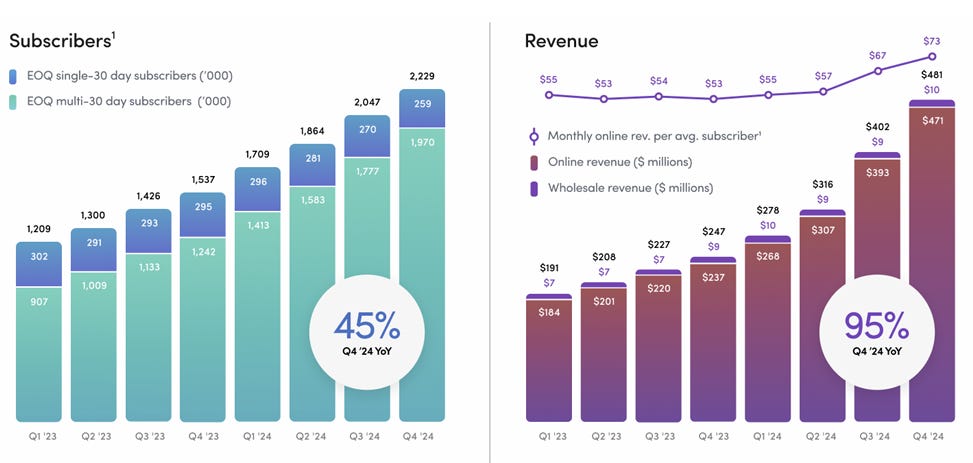

Over 2.2 million subscribers, growing at 45% annually - 4x increase from 12/2021 to 12/2024.

6x increase in subscribers using personalized offerings in two years to over 55%.

Founder-led, longer-term vision.

Recent acquisitions position HIMS for expansion into hormone and peptide therapy while increasing data-driven healthcare.

Now accepting HSA for weight-loss treatments.

2024 Earnings Release Highlights:

Hims & Hers continues to deliver exceptional growth, with revenue and profitability scaling rapidly.

Revenue Growth:

+95% QoQ in Q4 2024

+69% YoY for full-year 2024

Profitability of the company is growing.

Free cash flow is growing at a rapid rate. Note: HIMS applies a conservative approach, including web and app development in FCF calculations. Numbers may differ from DCF calculations in the valuation section.

Subscriber Growth: Increased to over 2.2 million+ from 1.5 million at year-end 2023.

Strong Balance Sheet: No long-term debt. Strong cash position.

Addressing the Impact of the Semaglutide Shortage Ending

On February 21, 2025, the FDA declared the semaglutide shortage over. This was big news for Hims & Hers, as it came just days before their earnings call. While the timing was unexpected, it ultimately worked in HIMS’ favor, allowing management to adjust guidance and directly answer difficult questions on the call.

What Was the Semaglutide Shortage, and Why Does It Matter?

Pharmaceutical companies are incentivized through patents. Since they devote so much research and development into creating new drugs, the companies are granted exclusive rights to sell patented drugs and recoup the costs of R&D. In this case, Novo Nordisk holds the patent for Ozempic (semaglutide/GLP-1) until 2031. However, if the drug (Ozempic) is in high demand and the company is unable to meet that demand, the FDA can declare a shortage. This shortage allows generic compounded versions of the drug to be sold by other companies (i.e. HIMS and GLP-1), even while under patent protection. A shortage is essentially a temporary allowance for other companies to help meet the demand of the drug and was never expected to be permanent.

With Novo Nordisk now claiming they can meet demand; the FDA has removed semaglutide from the shortage list. As a result, companies like HIMS can no longer sell compounded generics commercially.

However, there’s a legal loophole:

Semaglutide is commercially available in fixed doses (0.25mg, 0.5mg, 1mg, 1.7mg, and 2.4mg).

If a medication is unavailable in a specific prescribed dose, it can still be compounded and sold.

Since HIMS specializes in personalization, many of its GLP-1 prescriptions are in personalized, custom dosages. CEO Andrew Dudum has made it clear that while HIMS can no longer sell commercial dosages of GLP-1, that they will continue providing personalized prescriptions where clinically necessary.

CFO Yemi Okupe noted on the earnings call that:

“What we see in general in our platform is, as Andrew mentioned, many of the folks that are coming to our platform have come and have had struggles with GLP-1s in the past. That was the genesis behind one of the reasons behind why we very quickly looked to roll out the personalized dosages as well.

He also noted that “a majority of individuals on the platform today are utilizing personalized dosages versus the commercially available dosages.”

Example of HIMS GLP-1 Onboarding Regimen: Note the customized dosages.

The Financial Impact of GLP-1

My prior estimate for GLP-1 Revenue as of Q3 2024 was 10-15% of total revenue. The company has now confirmed $225 million in GLP-1 revenue for 2024, approximately 15% of total FY24 revenue.

Subscriber growth and revenue growth existed prior to GLP-1 announcements and offerings at HIMS. HIMS has been a disruptive and rapidly growing company before introducing GLP-1 into the equation.

Of note: GLP-1 was primarily a revenue and subscriber driver in the short term with compressed margins due to initial investment costs. The company has made it clear that economies of scale take time for new product lines.

Gross Margin Compression from 82% to 79.45% YoY. Expected per HIMS due to GLP-1.

I believe that GLP-1 ‘hype’ certainly fueled much of the recent stock craze surrounding HIMS but it was not, and has not been, a core tenet of my thesis for the investment. HIMS is well-positioned to adapt, already planning to:

Continue offering personalized GLP-1 dosages.

Bring back commercial GLP-1 with any new shortage.

Expand its weight loss portfolio, emphasizing its oral weight loss medications (already generating $100M+ in revenue within seven months of launch).

Introduce liraglutide as an alternative weight loss treatment in 2025.

While there will be customers that leave HIMS, many customers who initially joined for GLP-1 are expected to transition to other offerings.

Debunking the “No Moat” Argument

I disagree with the idea that HIMS lacks a competitive moat…

Brand & Marketing Moat

While I have been aware of HIMS since IPO, it first caught my attention as an investment opportunity due to its standout marketing strategy. HIMS has executed on a marketing strategy that has created a strong, trusted brand. Simply put, HIMS makes Erectile Dysfunction medicine “cool” rather than clinical or embarrassing.

HIMS has positioned itself with a first mover advantage in the personalized healthcare and wellness industry. Its focus on:

Personalized treatments

Combination medications

Direct-to-consumer accessibility

…makes it a unique player in the telehealth space.

Convenience & Consumer Experience

The U.S. healthcare system is a nightmare for many - complicated, expensive, and frustrating. Long wait times, insurance headaches, and unclear pricing leave patients feeling powerless. HIMS provides an alternative with a consumer-first approach that eliminates these barriers.

Accessibility – No waiting rooms. No insurance approvals. Just frictionless, direct-to-consumer care.

Discretion – Patients can access treatments privately and comfortably.

Transparent Pricing – Consumers know exactly what they’re paying before they commit.

Unlike traditional healthcare, where patients feel like passive participants, HIMS allows consumers to take control of their health.

The out-of-pocket cost of care continues to rise, with more Americans opting for high-deductible plans. As co-pays and other expenses grow faster than inflation, affordability is an increasing concern. HIMS is well-positioned within this cash-pay segment, offering upfront pricing and a premium experience.

From discreet online consultations to direct-to-door delivery, HIMS is designed for convenience. Consumers can browse treatments, receive personalized recommendations, and have medications shipped - all from their phone or computer. This retail-like approach makes healthcare as simple as shopping online, removing the stigma and complexity that often deter people from seeking treatment.

Unlike traditional telehealth models that feel transactional and impersonal, HIMS created a premium consumer engagement. Rather than passively following doctor’s orders, users customize their care, select treatments, and interact with a brand that prioritizes them.

In a world where convenience, transparency, and trust drive consumer decisions, HIMS offers a modern and approachable healthcare experience, a key differentiator.

I believe HIMS has and is continuing to grow their brand moat as a trusted, transparent, premium, personalized health and wellness provider that brings a consumer experience to the healthcare system.

Regarding Share Dilution: A Manageable Concern

HIMS has been diluting shares at about 8% per year, which isn’t ideal. It is important to understand that HIMS is a young, high-growth company that is utilizing Share Based Compensation to attract, retain, and incentivize talent. Free cash flow growth is rapidly outpacing share-based compensation. I believe the impact of Shared Based Compensation to be reasonable and manageable and will minimize over time.

2025 Outlook:

Growth Opportunities & Catalysts

Total Addressable Market (TAM): 100M+ Americans suffer from weight-related health problems.

New Categories: HIMS plans to launch 1-2 major new categories annually. Of focus with new acquisitions: low testosterone, menopause support, and peptides.

At-Home Lab Testing: New service offering that will support fricitionless access to hormonal treatment via HIMS while expanding personalized, data-driven care. Paired with MedMatch, HIMS' AI-driven treatment-matching service, at-home lab testing enhances the ability to identify additional products for consumer benefit. Utilizing data to personalize the consumer experience, increasing offerings and awareness of appropriate products based on data driven needs may lead to increased cross selling.

Subscription Growth: CEO Andrew Dudum aims for 10 million subscribers, a realistic target based on historical trends. On the earnings call, Dudum noted:

I think 10 million subs on the platform to me feels really quite in reach. And I think, frankly, pretty straightforward from a growth standpoint if you look at historical growth over the last five to six years. My optimistic hope and personally ambition would be to try to achieve this in the next five to six years.

In addition, average revenue per subscriber is becoming a larger driver of revenue growth:

While the addition of subscribers remains the primary component of our growth, monthly online average revenue per subscriber is becoming a more meaningful contributor as well. Monthly online average revenue per subscriber increased 38% year-over-year to $73 in the fourth quarter.

This is a positive long-term trend, though the recent spike was undoubtedly impacted by the sales of higher-priced GLP-1 products.

Risks & Challenges

Regulatory Risk: As always, there are regulatory risks for healthcare companies (and opportunities - i.e. favorable changes to compounding regulations).

GLP-1 Competition: Commercial semaglutide providers are working hard to limit access to compounded GLP-1. In addition, a direct-to-consumer cash option for Wegovy has been released but remains more than 2x the cost of HIMS offering. (Again, I see GLP-1 as a bonus here, not a core tenet of the HIMS thesis.)

Execution Risk: The recent FDA ruling on GLP-1 has put HIMS under increased scrutiny. Fortunately, the decision came before earnings, allowing the company to adjust its guidance and answer questions. Despite this, HIMS maintained a strong outlook, reflecting confidence in its execution of weight-loss products. While I’ve never viewed HIMS as purely a GLP-1 investment, it will be important to see how their estimations of personalized GLP-1 offerings and transition to aliterate weight loss products delivers.

If you're finding this content valuable, consider subscribing and sharing it with someone who might benefit.

You can also support me by buying me a coffee at: buymeacoffee.com/manuinvests!

Valuation:

Keep in mind that all of my calculations are estimates, intended to provide general guidelines for my personal decision-making.

Get a copy of my Valuation spreadsheet: Fundamentally Sound Valuation Spreadsheet

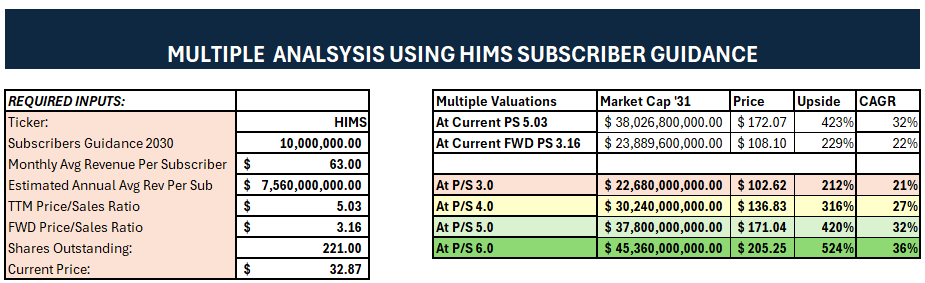

Multiple Valuation: Price/Sales

During the Q4 2024 earnings call, HIMS CEO Andrew Dudum reiterated confidence in the company’s long-term growth trajectory, stating that the goal of reaching 10 million subscribers was well within reach:

I think 10 million subs on the platform to me feels really quite in reach. And I think, frankly, pretty straightforward from a growth standpoint if you look at historical growth over the last five to six years. My optimistic hope and personally ambition would be to try to achieve this in the next five to six years.

With this target in mind, let’s look at a potential share price through the lens of the Price-to-Sales ratio, using Dudum’s stated goal alongside Monthly Average Revenue Per Subscriber (ARPU).

In Q4 2024, HIMS reported a Monthly ARPU of $73. However, this figure was temporarily elevated by GLP-1 prescriptions. We’ll use a more estimate number by using the full-year 2024 average, which was at $63 per subscriber per month.

Bullish/CEO scenario: By 2031, with 10 million subscribers generating $63 in monthly revenue per user:

Implied 2031 Price Range: $102.62 - $205.25. Average: $153.94

Implied Upside: 212% - 524%. Average: 368%

Implied CAGR: 21% - 36%. Average: 29%

Price for 3x Upside (~200% Gain): ~$51.00

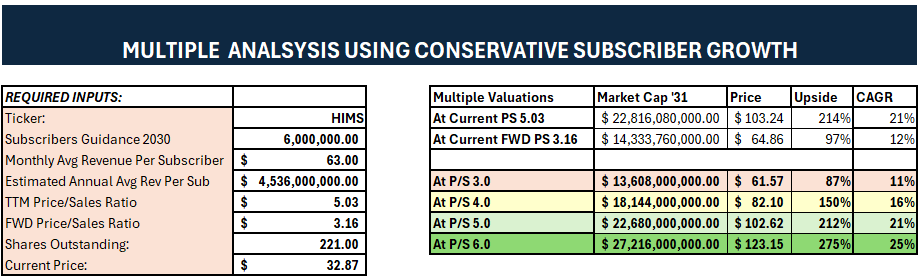

Conservative scenario: By 2031, with 6 million subscribers generating $63 in monthly revenue per user:

Implied 2031 Price Range: $61.57 - $123.15. Average: $92.36

Implied Upside: 87% - 275%. Average: 181%

Implied CAGR: 11% - 25%. Average: 18%

Price for 3x Upside (~200% Gain): ~$30.00

If we assume a bullish, yet reasonable Price-to-Sales ratio of 7.5…

Of note: HIMS currently has over 2.2 million subscribers, growing at an annual rate of 45%. The company has successfully scaled its subscriber base 4x from December 2021 to December 2024.

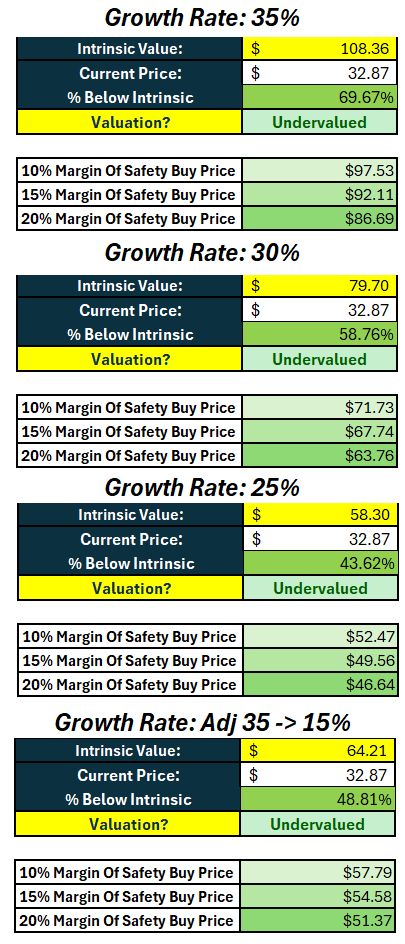

Discounted Cash Flow

At 35% Free Cash Flow Growth Rate, Terminal 3%.

Reflects we are undervalued at current price. 20% Margin of Safety is BUY at $86.69

At 30% Free Cash Flow Growth Rate, Terminal 3%

Reflects we are undervalued at current price. 20% Margin of Safety is BUY at $63.76

At 25% Free Cash Flow Growth Rate, Terminal 3%

Reflects we are undervalued at current price. 20% Margin of Safety is BUY at $46.64

At 35% Decelerating to 15% Free Cash Flow Growth Rate, Terminal 3%

Reflects we are undervalued at current price. 20% Margin of Safety is BUY at $51.37

DCF Valuation Summary:

Determination:

I believe HIMS is a great, fast-growing, yet volatile company that remains undervalued. I first invested after its initial quarter of profitability, starting at $12 and averaging up to $15.89 before Q4 earnings. Prior to Q4 earning, I felt a FV of HIMS was around $57 and was comfortable purchasing below $45. Following the post-earnings dip, I added in the mid-$30s, bringing my cost basis to $27.10.

Despite concerns over GLP-1, I see the reaction as overblown. My long-term conviction remains intact, and I continue to believe in 10x+ potential over the next decade.

Currently, HIMS is at my target portfolio weighting, but I’d consider adding more if the stock remains in the low-$30s to high-$20s. Based on a 20% margin of safety using a 25% free cash flow growth rate discounted at 10%, I view $46.64 and below as an attractive price. Purchasing in the low-$30s aligns with the more cautious 6 million subscriber scenario.

HIMS isn’t just a GLP-1 stock—it’s a disruptive healthcare brand. The business continues to scale, expand, and differentiate itself, making it a compelling long-term investment opportunity.

If you found this content helpful, please consider supporting with a subscription or by buying me a coffee at: buymeacoffee.com/manuinvests

Get a copy of my Valuation spreadsheet: Fundamentally Sound Valuation Spreadsheet

Disclaimer: The content shared on Fundamentally Sound is for informational and educational purposes only and should not be considered financial advice. Please do your own research before making any investment decisions.

Bonus: Q4 2024 Earnings Call Highlights

Key Insights from CEO Andrew Dudum

Data is a key differentiator on our platform as we are one of, if not the only, large scale vertically integrated health systems spanning the end-to-end patient journey. At the end of 2024, we began negotiations to acquire a provider of at-home whole body lab testing, which we were excited to close last week.

Whole body lab testing will also enable us to expand into specialties such as menopausal support, low testosterone, and more. With this acquisition, we are elevating the personalization of care individuals will be able to access on our platform. Expanding datasets enable us to identify elements of a member's health such as vitamin deficiencies and unoptimized health indicators leading to better personalization of treatment through expanded offerings that take these diagnostic components into account.

Almost 100 million Americans are currently struggling with weight loss.

At the end of 2024, we also signed an agreement to acquire a California peptide facility.

We believe this approach to personalized medicine will ultimately drive better clinical outcomes by enabling providers to personalize the dose, form factor, and other clinical delivery aspects of existing clinically validated medications. In our work, we are committed to integrity and transparency. We are not bypassing the regulatory process nor are we creating new drugs. The regulatory framework for compounding and the FDA have long recognized the need for compounders to be able to compound medication to meet patient needs that utilize ingredients of, but that are not essential copies of existing drugs. We focus on providing access to better care in this framework through personalization period.

Highlights from CFO Yemi Okupe

Revenue outside of our GLP-1 offering increased 43% year-over-year to $1.2 billion in 2024, reflecting an ability to achieve the floor of our revenue expectations for 2025 a year early.

Total subscribers on the platform increased 45% to over 2.2 million in the fourth quarter with over 55% of those subscribers subscribing to at least one personalized solution.

Gross margins declined approximately two points quarter-over-quarter in line with expectations highlighted earlier this year. The scaling of our GLP-1 offering as well as strategic pricing actions enacted within our GLP-1 offering in the fourth quarter are the primary drivers of this change. We expect margins to start to recover in the second quarter

Additionally, sterile capabilities provide a critical component necessary to expand into other areas such as menopausal support and low testosterone in the future.

we anticipate 2025 revenue contributions from our weight loss specialty of at least $725 million. This figure excludes contributions from commercially available dosages of semaglutide, which will not be offered on the platform after the first quarter. There may be the potential to offer commercially available dosages of compounded semaglutide throughout the year.

Q&A Highlights

I think 10 million subs on the platform to me feels really quite in reach. And I think, frankly, pretty straightforward from a growth standpoint if you look at historical growth over the last five to six years. My optimistic hope and personally ambition would be to try to achieve this in the next five to six years.

Oral offering continue to remain quite popular as a result of broader eligibility requirements, as a result of many consumers just being candidly more comfortable with the modality. And so as we look to what 2025 looks like, we do expect a continued meaningful contribution from our oral business. We're excited for liraglutide to come later this year.

Transition off GLP? Yes, that's a great question, Eric. I would suspect we will have to start notifying customers in the coming month and two that they will need to start looking for alternative options on the commercial dosing. Obviously, we have the expansive platform, whether it's the oral medication that are already out there or if there is some reason that this patient would qualify for some level of personalization that exists. But I would suspect, just being very direct, that a lot of those patients will try to go into the open market and try to secure a branded option in some form factors. So that transition is inevitable. I think that transition is going to have to take place and has been built into the guidance that Yemi provided.

Much of the increase in personalized subscribers that you're seeing that number drive north of 55% is driven in part by the continued shifting of subscribers to those categories.

How or why did you land at 10% for the discount rate in your DCF analysis?

Really strong article! Loved reading it!